Python Data Analysis Basics: Handling Stock Data with pandas

An introductory guide to loading, cleaning, and basic analyzing stock data using pandas in Python. The starting point for quant analysis.

Why pandas?

Handling stock data requires working with numbers sorted by date. While Excel can do this, it becomes slow and difficult to automate when dealing with tens of thousands of rows.

pandas is the standard library in Python for working with tabular data. It’s widely used in quant analysis, data science, and financial modeling.

Installation and Getting Started

pip install pandas yfinance matplotlib- pandas: data analysis

- yfinance: download free stock data from Yahoo Finance

- matplotlib: plotting charts

Loading Stock Data

Bitcoin Data from Yahoo Finance

import yfinance as yf

import pandas as pd

# Bitcoin daily data (2 years)

btc = yf.download("BTC-USD", period="2y")

print(btc.head())Sample output:

Open High Low Close Volume

Date

2024-04-08 69543.12 71842.15 68902.31 71015.94 32844900

2024-04-09 71015.94 71655.25 69241.84 69785.52 30492100

...Column explanations:

- Open: Opening price (first trade of the day)

- High: Highest price during the day

- Low: Lowest price during the day

- Close: Closing price (last trade of the day)

- Volume: Trading volume

Korean stock data

# Samsung Electronics

samsung = yf.download("005930.KS", period="1y")

print(samsung.tail())Basic Data Exploration

Checking data size

print(f"Number of rows: {len(btc)}")

print(f"Period: {btc.index[0]} – {btc.index[-1]}")

print(f"Columns: {list(btc.columns)}")Basic statistics

print(btc['Close'].describe())This provides mean, min, max, standard deviation, etc.

Filtering specific periods

# Data only for 2025

btc_2025 = btc.loc['2025']

# First quarter of 2025

btc_q1 = btc.loc['2025-01':'2025-03']Calculating Returns

A very common calculation in quant analysis.

Daily returns

btc['daily_return'] = btc['Close'].pct_change()

print(btc['daily_return'].tail())pct_change() computes the percentage change from the previous day. For example, 0.03 indicates a 3% increase, -0.02 indicates a 2% decrease.

Cumulative return

btc['cumulative'] = (1 + btc['daily_return']).cumprod()

print(f"Total return: {btc['cumulative'].iloc[-1] - 1:.2%}")Calculating Moving Averages

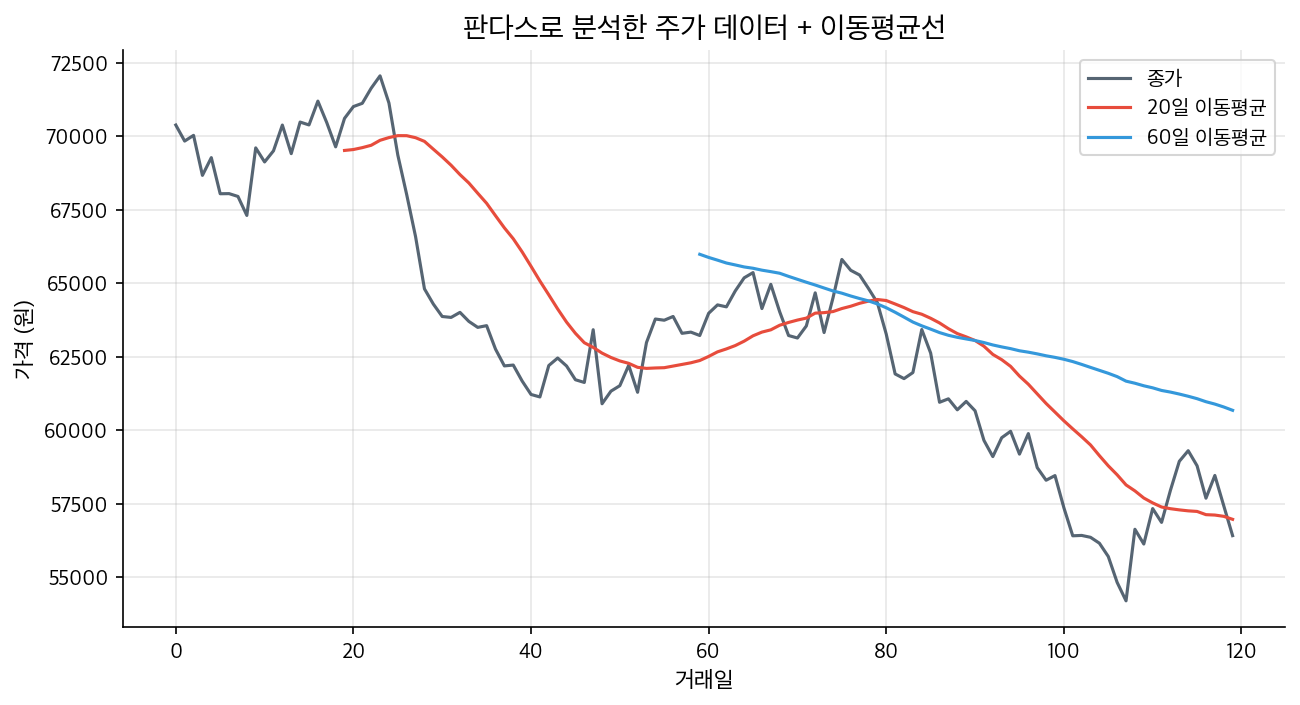

Moving averages smooth out price data by calculating the average over a set period. They are basic tools for identifying trends.

# 20-day moving average (short-term)

btc['ma20'] = btc['Close'].rolling(20).mean()

# 60-day moving average (mid-term)

btc['ma60'] = btc['Close'].rolling(60).mean()

# 200-day moving average (long-term)

btc['ma200'] = btc['Close'].rolling(200).mean()Finding Golden Cross / Dead Cross

# Golden cross: short-term MA crosses above long-term MA

btc['golden_cross'] = (

(btc['ma20'] > btc['ma60']) &

(btc['ma20'].shift(1) <= btc['ma60'].shift(1))

)

golden_dates = btc[btc['golden_cross']].index

print(f"Number of golden cross events: {len(golden_dates)}")

for d in golden_dates[-5:]:

print(f" {d.date()}")Plotting Charts

Close price + Moving Averages

import matplotlib.pyplot as plt

plt.figure(figsize=(14, 6))

plt.plot(btc.index, btc['Close'], label='Close Price', linewidth=1)

plt.plot(btc.index, btc['ma20'], label='20-day MA', linewidth=1)

plt.plot(btc.index, btc['ma60'], label='60-day MA', linewidth=1)

plt.title('Bitcoin Daily Chart')

plt.xlabel('Date')

plt.ylabel('Price (USD)')

plt.legend()

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.savefig('btc_chart.png', dpi=150)

plt.show()Daily returns distribution

plt.figure(figsize=(10, 5))

btc['daily_return'].hist(bins=100, alpha=0.7)

plt.title('Bitcoin Daily Return Distribution')

plt.xlabel('Daily Return')

plt.ylabel('Frequency')

plt.axvline(0, color='red', linestyle='--')

plt.tight_layout()

plt.show()Common pandas functions summary

| Function | Example | Usage |

|---|---|---|

| Add column | df['new'] = df['Close'] * 2 | Create new indicators |

| Filtering | df[df['Close'] > 70000] | Conditional selection |

| Sorting | df.sort_values('Volume') | Sort by volume |

| Grouping | df.groupby(df.index.month).mean() | Monthly averages |

| Handling missing data | df.dropna() | Remove NaNs |

| Saving | df.to_csv('data.csv') | Save to file |

Next Steps

Working with pandas is the foundation of quant analysis. From here, three main directions are suggested:

Implementing Technical Indicators: Calculate and visualize RSI, MACD, Bollinger Bands, etc.

Backtesting: Develop trading rules and test their performance against historical data.

Automated Trading: Connect to exchange APIs for real-time trading automation.

No matter which path you choose, pandas will be a core tool. Mastering these basics will make advanced steps much easier.

Recommended Articles

What is an LLM Agent? Easy guide from concept to quant investment applications

RunPod vs Vast.ai: Practical comparison of local LLM and backtest GPU rental

Bitcoin News Sentiment Analysis: Techniques to read market psychology and investment strategies

Related Posts

Newsletter

Weekly Quant & Market Insights

Get market analysis, quant strategy ideas, and AI & data tool insights delivered to your inbox.

Subscribe →